Insurance Protocols — The Rise of Cautious Investors

Insurance Protocols — The Rise of Cautious Investors

Source: Flaticons

In my private circles, I have stated that I feel strongly that 2022 would be the year Insurance protocols focusing on serving the DeFi community should start having the spotlight. I have two main reasons for making this prediction.

As cryptocurrency markets mature, participants would want to engage in practices that ensure their capital is protected. I firmly believe that the insurance sector that serves decentralized finance protocols should grow as the nature of participants evolve.

I anticipate regulation of cryptocurrency markets this year, with emphasis on cryptocurrency custodians and stablecoin issuers - both algorithmic and fiat-backed stablecoins. Already the Thailand SEC is proposing cryptocurrency custodian regulations. I expect regulators globally to make several attempts to separate the duties of market makers and custodians within the cryptocurrency markets. Also, bills like the Digital Asset Market Structure and Investor Protection Act and The Stablecoin Tethering and Bank Licensing Enforcement (STABLE) Act are being discussed in the United States Congress regarding Stablecoin regulations.

Upon regulation, I expect massive inflows from institutional investors who would almost surely emphasize the safety of funds deployed.

Currently, less than 2% of the total value locked in DeFi protocol is insured. This gives room for plenty of growth as Insurance protocols try to gain a more significant market share.

I have been exploring several insurance protocols to pick out potential investments with these two key points, and I will share some of my findings in this and subsequent newsletters.

Current insurance models

Blockchain made trustless and borderless insurance models highly feasible. Several insurance companies and protocols have sprung up through the years, solving insurtech problems in several domains. Currently, four broad methods of insurance are being implemented around blockchain projects.

Model 1 — Self-Insurance

This model is when ecosystems take steps to protect the protocol. A blanket coverage would cover the ecosystem and every member of the community automatically upon signing up. The ecosystem sets aside a pool of funds dedicated explicitly to insuring users against exploits and losses. For example, Alex Mashinsky of Celcius announced a self-insurance plan for all users of celsius.

Model 2 — Insurance via a Mutual or Cooperative Approach

This is the most widely used approach in Decentralised Finance. Nexus Mutual was the pioneer of this approach and its application in DeFi. Other notable protocols using this approach include Insurace and Bridge Mutual.

Model 3 — Parametric Insurance

This insurance model is designed only to issue a predetermined payout based on clearly specified outcomes. Thus the party seeking to be insured pays for cover and receives a quotation from the insurer that determines the total payout if the trigger events occur. Arbol is an example of a company utilizing the parametric insurance model.

Model 4 — Traditional Insurers attempting to cover abstract assets.

Traditional insurers that adapt their services to intangible/abstract assets have also become a popular model. This insurance method typically involves contacting the insurer to underwrite the risk and specify all terms. Evertas Insurance is an example of a traditional insurer adapting to intangible digital assets.

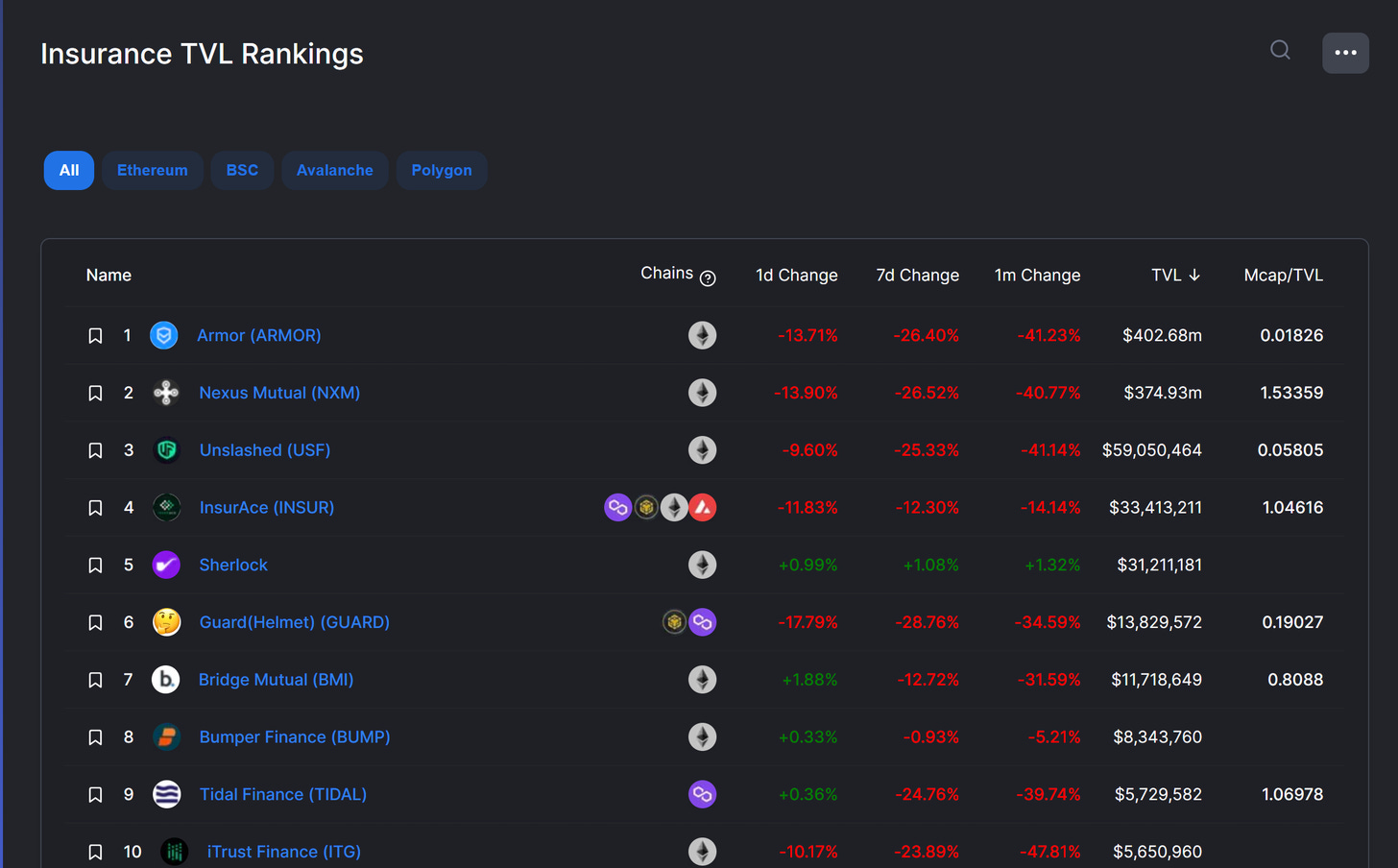

Prominent DeFi Insurance Protocols

Source: DefiLlama

Some personal thoughts

When I was conducting my research about the most viable investments to make in the DeFi insurance space, I considered several factors, including:

Multi-chain compatibility.

Has the protocol been audited?

Ease of onboarding and KYC requirements.

Payout mechanisms to claimants.

Considering these factors, I have a high affinity towards the Insurace protocol. Insurace is a multi-chain protocol with extremely cheap premiums. The protocol has been performing very well in terms of growth of the value of cover sold. The token is currently down to $0.7 from its highs of $16.84. In a subsequent newsletter, I will be diving into how Insurace works; I believe they are poised for growth soon. I also must mention three other protocols: Sherlock, Amour, and Nexus Mutual; these are also very innovative insurance protocols offering excellent services.

It is also essential to monitor insurance protocols that are working to become embedded in several of the most prominent DeFi protocols. These partnerships prove to be one of the critical strengths of Nexus Mutual, and I expect to see more of these insurance protocols work to become embedded within DeFi projects.

Insurance protocols that cling on to as many relevant DeFi protocols at source would dominate market share and provide investors splendid returns.

Don’t forget to hit me up on Twitter or drop a comment if you have any thoughts on this.

Thanks.